KMS Technology has joined hundreds of insurance and insurtech leaders at the InsurTech America Symposium 2026. Our CTO, Guy Merritt, participated as a featured panelist on “The Future is Coming Fast and Furious,” a session focused on AI, risk, and the future of insurance operations that set an apt tone for the entire event. Insurance modernization is no longer limited to upgrading policy, claims, or billing systems. It now requires insurers to align AI, data foundations, core architecture, governance, and workforce transformation around a shared operating model.

At this year’s InsurTech America Symposium, one thing quickly stood out: the conversation has matured. Across its agenda, expert tracks, and speaker lineup, the event centers on the real work of transformation: modernizing claims, underwriting, product innovation, and the data infrastructure that makes it all possible.

Here are the five themes that cut across the most compelling conversations at InsurTech America Symposium 2026, along with what they mean for insurance organizations trying to act.

01. AI Governance Is Now a Core Insurance Modernization Requirement

The most striking shift from prior years was the near-total absence of exploration language. Practitioners from across the industry were no longer debating whether to deploy AI. They were comparing notes on what breaks when you do. Autonomous AI agents initiating claims tasks, routing underwriting decisions, and coordinating cross-system workflows are in live production environments right now, across a broader range of carriers than most would have expected a year ago.

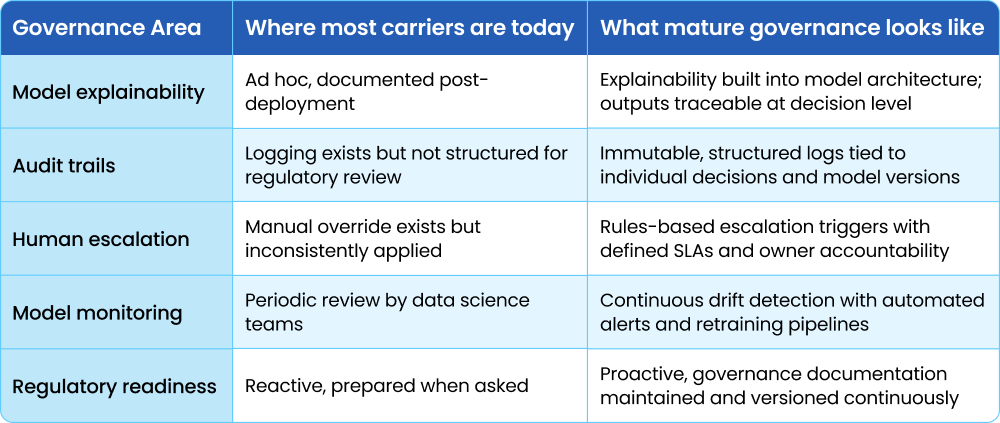

The conversations that drew the most engagement were about the infrastructure around it. Guardrails, audit trails, explainability layers, model monitoring, human escalation paths. The carriers further along consistently described the same lesson: building the AI model is the straightforward part.

Building the governance architecture that keeps it trustworthy in production, under regulatory scrutiny, and across the full range of edge cases. That’s where the real engineering effort lives, and where most organizations underestimate the work ahead of time.

Regulators made clear this is no longer a future concern. State insurance commissioners and rating agency representatives at the event were explicit: model risk management, pricing transparency, and algorithmic fairness are active areas of oversight today.

For carriers, this is a sign to build governance from the start rather than retrofit it after the fact. Organizations that treat explainability and auditability as first-class engineering requirements, not compliance paperwork, will move faster and with more confidence as the regulatory environment tightens.

AI governance: where carriers stand and what’s required

02. Data Foundations Are Still Blocking Insurance Modernization

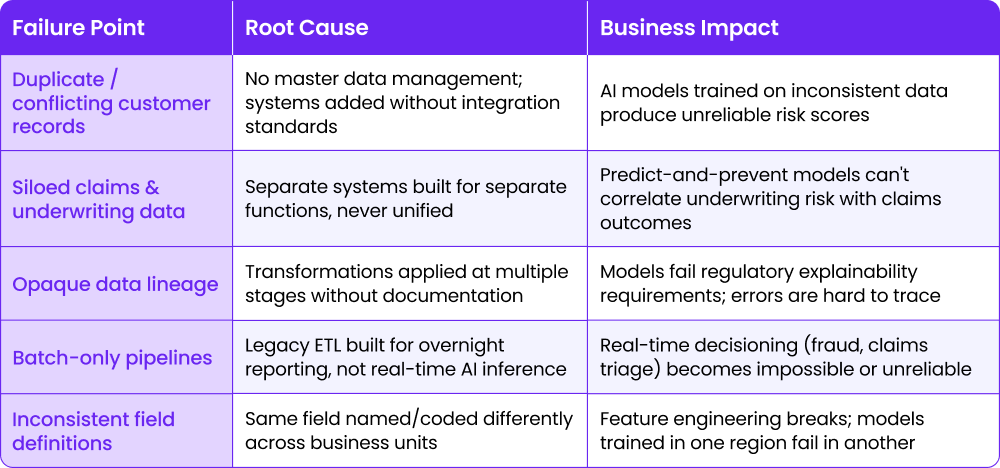

Across the underwriting, technology, and claims tracks, a consistent frustration surfaced: organizations are investing heavily in AI capabilities while their underlying data architecture remains a patchwork of legacy schemas and disconnected systems.

The most candid conversations weren’t about AI at all. They were about entity resolution, data lineage, and the basic challenge of getting reliable, consistent data out of systems that weren’t designed to talk to each other.

The practitioners most advanced in their AI deployments shared a common thread: they had made deliberate, often unglamorous investments in data infrastructure before scaling intelligent systems on top of it:

- Clean data models

- Consistent definitions enforced upstream.

- Pipelines designed for AI consumption.

The carriers still in early innings were often discovering mid-project that the data they assumed existed in usable form didn’t, or existed in six different forms across three systems with no clear owner.

Senior data and technology leaders also raised the gap between operational data and strategic insight. The ability to transform fragmented signals (underwriting, claims, market, and customer data) into prioritized, board-level risk intelligence is increasingly a differentiator. But it requires a foundation that most carriers haven’t fully built.

Common data failure points in insurance AI programs

For technology partners, this is one of the most consequential places to engage: helping a carrier get its data architecture right directly determines the ceiling of every AI investment that follows.

03. Insurance Core Modernization Is Moving Beyond Big-Bang Replacement

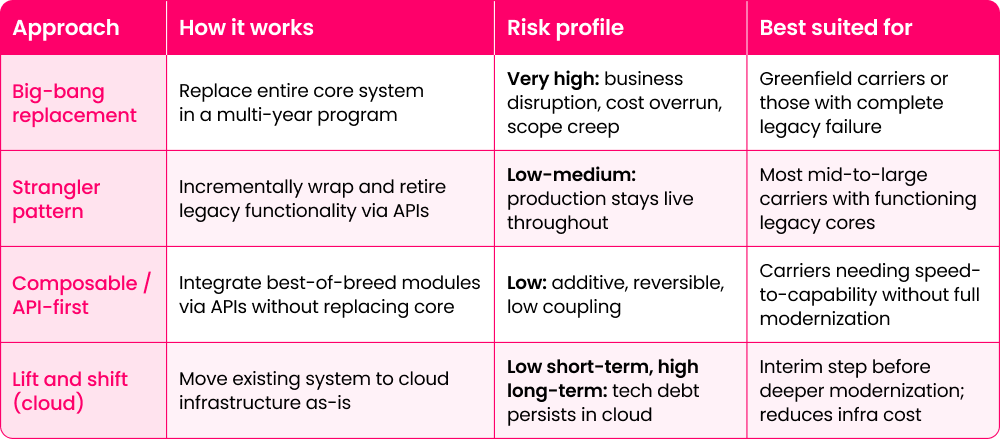

There was a clear consensus among the technology and operations leaders in the room: the all-or-nothing core system replacement has lost credibility.

Carriers have watched enough multi-year, nine-figure transformation programs end in write-downs to know that wholesale replacement is rarely the right answer for a business that needs to stay in production while it modernizes. The question isn’t whether to modernize core systems; it’s how to do it without putting the business at risk.

What’s replacing the big-bang approach is a composable, API-first, incremental model. Carriers are wrapping legacy systems with APIs, retiring functionality piece by piece using the strangler pattern, and integrating best-of-breed components where they deliver clear value.

The emphasis on API-first architecture was notable: it enables carriers to swap components, integrate new capabilities, and modernize at a pace the business can absorb, rather than forcing a synchronized cutover that touches everything at once.

Modernization approaches compared

A theme that recurred across multiple sessions: activity isn’t progress. Organizations that treat modernization as a series of technology purchases consistently end up with a more expensive version of the same complexity.

The carriers making real headway are the ones treating modernization as an architectural program with deliberate sequencing, clear value thresholds for each phase, and engineering discipline that keeps the system coherent as it evolves.

04. Insurance Modernization Is Shifting From Reactive to Predictive Operations

The event keynote set this up explicitly, and it ran through conversations across every track: insurance is undergoing a structural migration from paying for loss to preventing it.

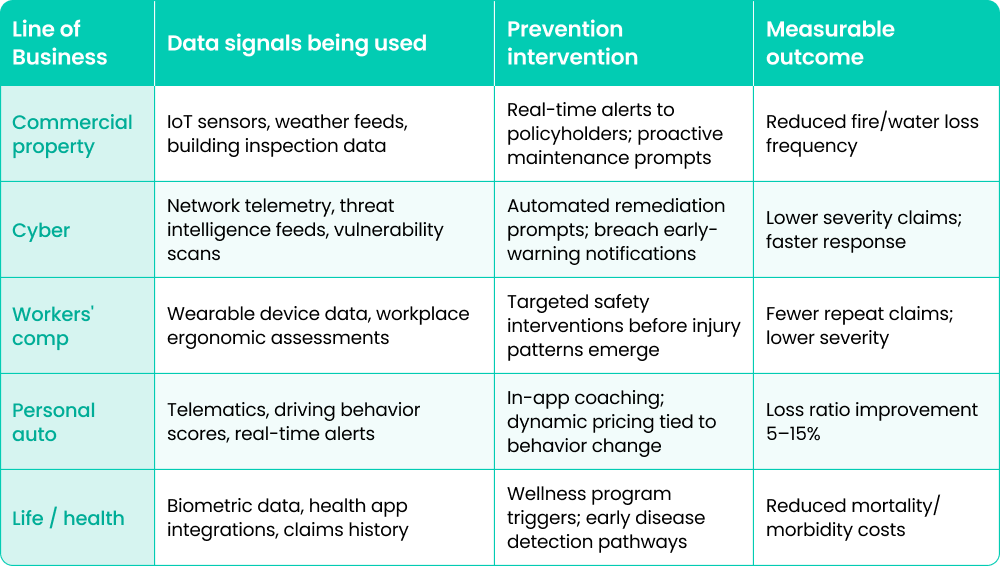

Carriers are embedding predictive analytics, IoT data, real-time monitoring, and behavioral signals into their core offerings, turning risk mitigation from a value-add into a product in its own right. Major carriers in property, commercial, cyber, and life segments described live implementations where intervention happens before the claim, not after.

For underwriters, this changes the inputs. Models now need to incorporate signals that didn’t exist in underwriting workflows five years ago: environmental data, device telemetry, behavioral patterns, real-time risk scores. The challenge isn’t just accessing that data; it’s integrating it into decisioning processes in a way that’s auditable, explainable, and consistent with governance requirements. The sessions on this topic surfaced a recurring tension between the speed at which new data sources become available and the organizational readiness to use them responsibly.

For claims, the shift means triage and segmentation need to happen faster and smarter at the first notice of loss. Practitioners described how AI-driven initial routing compounds in value across the entire lifecycle. But the technology implication is significant: operationalizing predictions requires real-time data pipelines, and the engineering infrastructure to turn a score into an automated action reliably, at scale, within compliance boundaries.

Predict-and-prevent: Use cases by line of business

05. Insurance Modernization Depends on Organizational Change, Not Just Technology

For all the technical depth across two days of sessions, some of the most honest conversations were about people and organizations, not systems.

A recurring theme across the innovation and digital experience track was the gap between digital ambition and organizational reality: carriers are buying new capabilities faster than their structures, incentives, and workflows can absorb them. Digital-first isn’t a technology posture but an organizational redesign, and most transformation programs underestimate how much of the work lives there.

Technology deployments often fail because the workflows weren’t redesigned around the new capability, the people closest to the process weren’t involved in shaping the solution, and change management was treated as an afterthought rather than a core workstream. Practitioners who had navigated this well described a common pattern: deliberate investment in the organizational side, including dedicated funding, governance structures, and explicit permission to experiment and fail small.

There was also a candid conversation about talent. Building a digital-first insurance organization requires attracting and developing people who see insurance as a technology career, and that’s a harder sell than most carriers have historically made.

The organizations making progress are being intentional about how they present themselves to talent: what the work looks like, what the growth path is, and how technology roles connect to the business problems that make insurance meaningful. It’s a long-term challenge, but it starts with decisions made now.

What Insurance Modernization Requires Next

InsurTech America Symposium (IAS) 2026 made one thing clear: the window for deliberation is closing. The carriers building durable advantages right now are pairing strategic clarity with strong engineering execution. They are moving fast enough to matter, carefully enough to last.

Across governance, data, modernization, predictive capability, and organizational change, the gap between carriers who are acting and those still planning is widening every quarter.

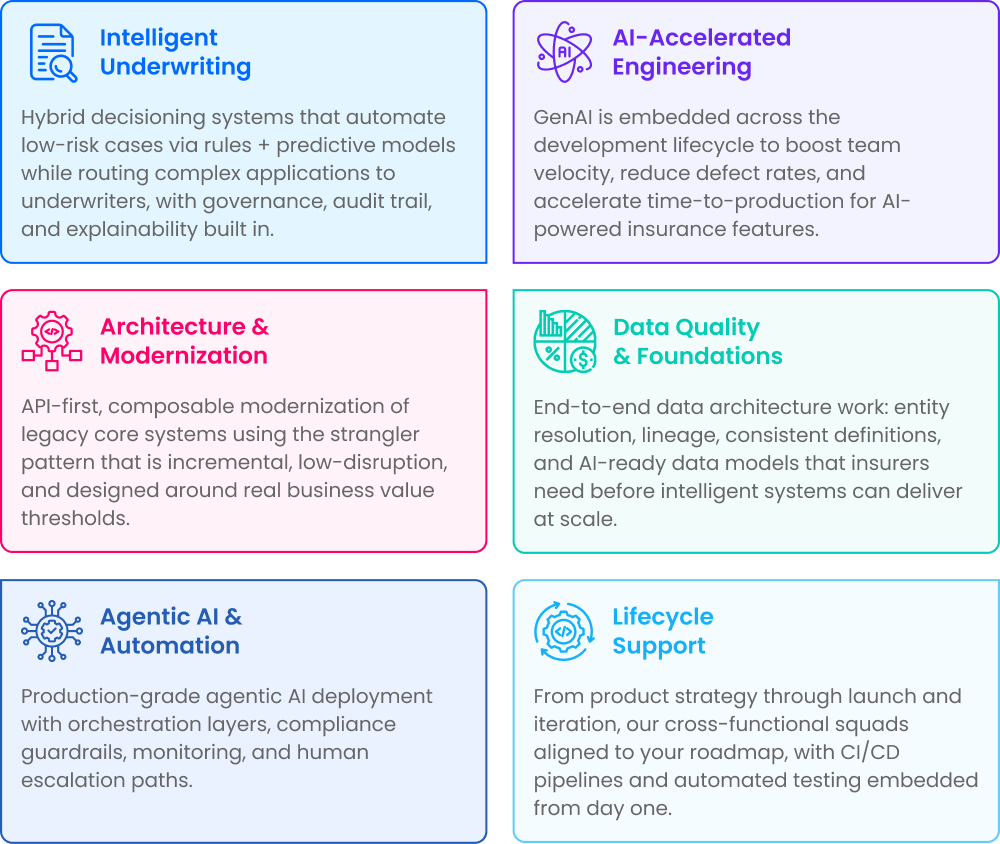

KMS Technology is an AI-native engineering firm that has worked alongside insurance carriers and insurtech organizations for 17+ years, from carriers to MGAs to distribution platforms. We bring the depth to match the complexity that InsurTech America Symposium (IAS) 2026 surfaced across every track.

If your organization is navigating any of these shifts, our experts at KMS Technology would welcome the conversation.