The insurance industry has reached a turning point. AI has moved from experimentation to expectation, becoming a core priority at the executive level. What was once explored in innovation labs is now embedded in boardroom discussions, with clear pressure to deliver measurable results. AI in insurance is no longer defined by whether carriers can launch use cases.

The real differentiator is whether those use cases can scale into measurable improvements in claims, underwriting, customer operations, and enterprise performance.

But while investment and adoption are accelerating, outcomes are not keeping pace.

Carriers are building, piloting, and deploying AI at pace. But many are still struggling to translate that momentum into tangible business value. This widening gap between AI activity and AI impact is now the defining challenge for insurance executives in 2026.

This article examines where insurance carriers truly stand in their AI journey today, unpacks the growing gap between investment and real impact, and outlines the practical steps executives must take to turn AI into measurable business value.

AI in Insurance: Where the Industry Actually Stands in 2026

57%

of insurance executives have both generative and agentic AI as top tech investment priorities for 2026.

Source: PwC, 2025

AI is now a boardroom-level mandate

With a significant majority of insurance CEOs prioritizing AI as a top investment focus, carriers are committing substantial budgets to initiatives expected to generate returns within the next few years. For insurance carriers, the challenge is shifting from AI investment to a repeatable model for measuring AI impact across business functions.

AI adoption is reshaping core insurance operations

Insurers are scaling AI across underwriting, claims, onboarding, and customer service, with growing expectations that next-generation, agentic AI will redefine how these functions operate at their core.

Governance and ethics are slowing adoption

Challenges around bias, fairness, and transparency continue to act as major barriers, pushing insurers to invest in stronger governance frameworks, model oversight, and explainability.

Workforce transformation is becoming urgent

As AI capabilities become critical to growth, organizations are accelerating upskilling efforts, refining hiring strategies, and redesigning roles to align with an AI-enabled future.

AI is unlocking growth, while amplifying cyber risk

While AI is driving efficiency, modernization, and innovation, it is also increasing exposure to cybersecurity threats, making risk management a central concern in scaling AI.

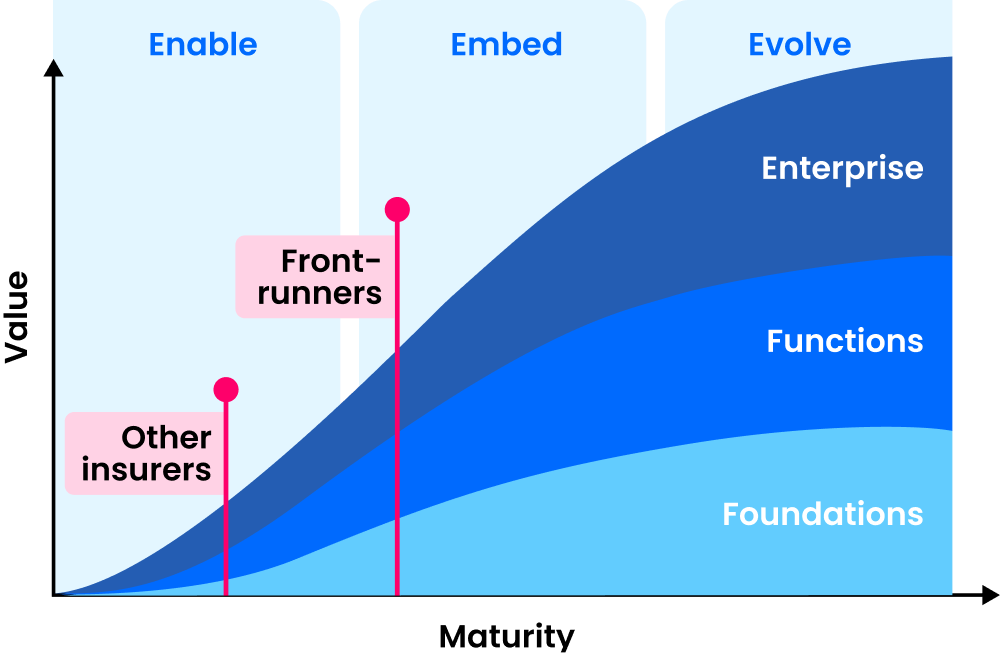

The AI in Insurance Gap Between Leaders and Laggards

KPMG’s AI Value Model, 2025

To understand how insurers are progressing, we need to look at AI through a three-phase value model, moving from foundational readiness to enterprise-wide transformation.

Enable

The focus is on building the foundation. Organizations define their AI strategy, establish governance, upskill teams, and launch initial use cases using existing platforms and pretrained models.

Embed

AI is integrated into core workflows. Insurers redesign processes, deploy AI at scale, and align technology, data, and workforce capabilities to drive measurable operational value.

Evolve

AI becomes a driver of business innovation. Carriers transform operating models, unlock new value across ecosystems, and combine AI with emerging technologies to create new products and growth opportunities.

Front-runners are scaling AI as an operating capability

A clear tier of insurers has emerged: carriers who have moved decisively beyond proof-of-concept territory and are now deploying AI use cases in production that deliver tangible business outcomes.

These front-runners invest simultaneously in two things most carriers treat as sequential.

They build the AI foundation and embed AI into live business processes at the same time, rather than waiting for the foundation to be “ready” before pursuing value.

Their focus is on end-to-end processes, not isolated tasks. They are redesigning underwriting workflows, automating claims triage, scaling scarce expertise through AI-assisted decision support, and converting unstructured data like call recordings and scanned documents into actionable intelligence.

Some are approaching scale across specific business units, and they are actively accelerating, making the gap with everyone else more difficult to close.

The Majority Are Still Catching Up

Most carriers fall into a middle category. They have deployed at least some AI in production like internal productivity tools, Copilot-style assistants, or a handful of individual use cases, but their approach remains fragmented.

Investments tend to follow individual use cases rather than a coherent process redesign. Foundation work (data, technology, governance, organizational capability) is addressed reactively, driven by the needs of the next use case rather than a strategic architecture.

This creates a hidden constraint. While progress is visible, it does not compound. Without structural alignment, gains remain localized, and scaling becomes increasingly difficult.

The Emerging Group Faces a Harder Problem

At the lower end of the maturity spectrum, some carriers remain in early stages, typically smaller organizations or those carrying heavier transformation backlogs.

They have limited AI activity, few or no production use cases, and a foundational infrastructure that is not yet ready to support meaningful AI deployment. For these carriers, the challenge is not just technical. It is also about making the business case internally, in environments where other strategic priorities compete fiercely for capital and attention.

The risk for this group is not only falling behind on AI, since they already have. As front-runners accelerate their AI operating models, the cost and complexity of catching up increases.

The Honest Performance Gap: AI Activity vs. AI Impact

Value is present, but difficult to quantify and scale

When asked whether AI is delivering value, most insurers answer yes. But the follow-up question reveals the problem: almost no one can point to clear, quantified evidence of that value.

No carrier in recent research reported receiving significantly more than expected from AI. Many acknowledged that while the benefits feel real, they are difficult to translate into measurable financial terms like cost reductions, headcount impact, revenue uplift.

The reasons are partly structural. Many carriers are still in early production stages, and the returns from process-embedded AI compound over time rather than arriving immediately. But the absence of measurement is itself a strategic gap.

Carriers that cannot track the impact of their AI investments are flying blind when it comes to prioritization, resource allocation, and making the case for further investment to boards already weighing competing demands.

Local optimization is limiting enterprise transformation

Most carriers have established AI productivity targets, but nearly all of them are local: specific use cases, specific departments, or specific processes. Very few have set organization-wide targets that hold business unit leaders accountable for AI-driven improvements.

This localized approach reflects where most carriers are in their maturity journey. It is not wrong as a starting point. But as AI matures, the absence of enterprise-level performance accountability creates a ceiling.

The carriers generating returns at scale are those who have moved beyond isolated metrics toward integrated measures of AI value across their operations.

Strategic ownership of value becomes the real problem

It would be easy to frame the measurement gap as a data infrastructure problem. However, it is indeed a strategic leadership problem.

When AI value tracking sits outside core business ownership like P&L owners, business unit leads, and CFOs, it loses the organizational weight needed to drive action.

The carriers closing the activity-to-impact gap are those who have made value tracking a central element of their AI governance.

Where Insurance Companies Are Investing in AI

Efficiency still dominates AI investment

Across the industry, efficiency improvement remains the dominant rationale for AI investment. Carriers are using AI to automate repetitive administrative tasks, reduce manual touchpoints in claims and underwriting, and free up skilled employees for higher-value work.

This is economically rational. Cost ratios are a persistent competitive pressure in insurance, and AI offers a credible path to structural cost reduction.

The efficiency agenda spans a spectrum of sophistication. At the simpler end, personal productivity tools and AI-assisted drafting help employees move faster on everyday tasks.

At the more advanced end, carriers are redesigning entire processes around AI capabilities: combining document digitization, sentiment analysis, summarization, and decision support into integrated workflows that fundamentally change how work gets done.

Advanced use cases are reshaping workflow

Three categories of more advanced GenAI use are beginning to emerge. These include:

- Process redesign: where multiple AI capabilities are combined to reimagine how an end-to-end workflow operates, rather than simply automating a single step within it.

- Digitizing analog information: converting phone calls, physical archives, and unstructured correspondence into structured data that can feed downstream AI systems and improve straight-through processing rates.

- Scaling scarce expertise: using AI to extend the reach of highly specialized and expensive human capabilities, such as legal analysis, subrogation assessment, or complex risk modeling.

The transformation agenda is still largely missing

For all the activity, one finding stands out for what is absent: very few carriers are investing meaningfully in transformative use cases – AI applications that would create new business models, new products, or new customer value propositions.

The focus is almost entirely on improving what already exists. This reflects a pragmatic and defensible choice in the short term, but it also carries strategic risk. Hence, the carriers who figure out how to use AI to create new sources of customer value will have advantages that are harder for competitors to replicate than pure efficiency gains.

The efficiency agenda raises the floor for everyone. The transformation agenda is where sustainable differentiation gets built.

Four AI Foundations Insurance Carriers Need to Strengthen

Data

The Most Underinvested Layer

Data is consistently identified as the most challenging element of the AI foundation, and consistently the most underinvested.

Most carriers have made progress on data governance in the context of regulatory requirements like Solvency II and IFRS 17, but these frameworks focus primarily on financial and actuarial data. The operational data that AI requires must be unstructured, diverse, continuously updated, and governed in ways that satisfy the EU AI Act. Unfortunately, these datasets are largely outside the scope of existing data management practices.

AI use cases that depend on poor-quality or inaccessible data either underperform or require expensive and time-consuming remediation. Carriers that invest in data infrastructure ahead of use case demand find themselves able to move significantly faster when the use case opportunity arrives.

Technology

Choices Get More Consequential

Most carriers have built a reasonably stable technology environment, but the transition to generative and agentic AI is exposing new gaps.

Standard GenAI tools and platforms are widely deployed, but the architectural decisions that will determine carriers’ ability to scale AI are becoming more consequential. These choices include cloud infrastructure, API connectivity, data platform design, and the build-versus-buy calculus for custom use cases.

The carriers who will scale AI most effectively are those making deliberate, forward-looking technology choices now, rather than accommodating AI use cases one at a time within existing architectures.

Organization

The Human Change Problem

As AI matures from experimentation to production, the dominant challenge shifts from technical to organizational.

Deploying a use case and getting real business value from it are different problems. The latter requires process redesign, change management, business buy-in, and new ways of working. This is where most AI programs stall.

The business functions that consume AI outputs are often not sufficiently involved in designing them. Product owners, business analysts, and operational managers who understand processes deeply are in short supply across the industry. The AI capabilities sitting in central technology and data teams often cannot translate into lasting business impact without this human bridge.

Capability

Business Teams Are the Weakest Link

Senior technology and data teams in most carriers have adequate AI capabilities. The gap is in the business.

AI literacy is the ability to understand what AI can and cannot do, to identify use case opportunities, to critically evaluate AI-generated outputs. However, this ability is significantly insufficient across operational functions for the scale of transformation that is now underway.

Carriers investing in role-based AI training, AI leadership programs for senior management, and bottom-up mechanisms that allow employees to surface AI use case ideas are building a compounding advantage.

The Workforce Reality: Everyone Will Be Affected

AI is forcing a fundamental rethink of processes

AI does not simply improve existing processes, but also requires them to be redesigned. The right question has shifted from “how do we add AI to this workflow?” to “what is the best way to accomplish this outcome, given what AI, humans, and automation?”

This is a more ambitious change agenda than most carriers have fully internalized. Process redesign at scale requires deep operational knowledge, significant investment in change management, and a willingness to question established ways of working.

It also takes longer and is harder to measure than deploying an individual use case, which is partly why many carriers are not yet doing it.

Workforce impact remains under-explored

Most carriers have not yet developed a clear, quantified view of what AI will mean for their workforce.

The more mature carriers have begun analyzing the impact at the level of specific business units or role types, and some have started to incorporate this analysis into budgeting and hiring decisions. But for the majority, the workforce impact question remains open.

This gap matters for several reasons. It limits carriers’ ability to plan reskilling and transition programs with any precision. It makes it harder to have honest conversations with employees about what AI means for their roles, creating anxiety that undercuts adoption. And it leaves carriers exposed when the impact does arrive, without the organizational preparation needed to manage it well.

The carriers that will navigate this transition most effectively are those who start the workforce impact analysis now, before the pressure becomes acute.

Use the employee sentiment wisely

Employees at most carriers appear to hold a positive view of AI. They see it, at least for now, primarily as a tool that will support their work rather than replace it. This is a significant asset for carriers who want to drive adoption, and it reflects the current reality that most AI investment is focused on augmentation.

However, this sentiment is fragile. It depends on AI actually delivering on the promise of making work better, not just making organizations more efficient. Carriers that use AI primarily as a cost-reduction mechanism while neglecting the employee experience are likely to find that goodwill erodes.

What Insurance Executives Should Do Right Now

Close the Measurement Gap Immediately

If your organization cannot clearly articulate the financial value your AI investments have generated, that is the first problem to solve. Not because the value is not there, but because without measurement, you cannot prioritize, cannot make the case for further investment, and cannot hold business leaders accountable. Establish a value tracking function with teeth that are owned by business leaders, not by technology teams.

Invest in Data Before the Use Case Demands It

The most common pattern of regret among more mature carriers is waiting too long to address data infrastructure. Data quality, governance, accessibility, and AI-readiness are slow-moving capabilities to build. Starting now, even before specific use cases require it, reduces the drag on every AI initiative that follows.

Build Foundation And Use Cases in Parallel

The front-runners are not building a perfect foundation and then deploying use cases. They are doing both simultaneously, using use case needs to inform foundation priorities and foundation improvements to enable better use cases. If your AI program is treating these as sequential, you are accepting unnecessary delays.

Shift Ownership to The Business

AI that lives inside technology or data teams rarely generates the business value it could. The transition from AI activity to AI impact requires business function leaders to own AI outcomes in their domains. This means involving them in use case design, holding them accountable for adoption, and measuring AI performance against business metrics, not technical ones.

Redesign Governance for Speed

Review your AI risk and governance processes with a specific question: are these processes calibrated to the actual risk profile of each use case, or are they applying a uniform level of scrutiny to everything?

For lower-risk applications, streamlined processes should be the norm. The governance investment should be concentrated where AI decisions carry real consequences for customers, for fairness, and for regulatory compliance.

Start the Workforce Impact Analysis Now

Waiting until AI use cases are in production to think about workforce impact is too late. The analysis of which roles, which tasks, and which capabilities will be most affected by AI needs to happen in parallel with the AI deployment roadmap. Understand how roles will evolve and prepare the organization ahead of time.

The Window Is Open, But Not Forever

The insurance carriers most likely to lead in an AI-defined competitive landscape are not necessarily the ones that move fastest. They are the ones who build the most capable, well-governed, and deeply embedded AI operating models. The momentum is to improve continuously rather than deliver a one-time productivity bump.

That is the work of the next phase. And for carriers willing to do it with discipline, clarity, and honest accountability, the opportunity is substantial.

At KMS Technology, we partner with insurance carriers to move beyond experimentation and turn their AI ambitions into real business outcomes through scalable engineering, strong data foundations, and AI-native operating models.

If you’re looking to close the delivery gap, let’s start the conversation.